CLEAN HYDROGEN PRODUCTION TAX CREDIT, EXPLAINED PART 5

Federal income tax credits in the United States are not all created equal.

Some credits can be bought and sold, whereas others can’t. Some credits are refundable, but most are not. Some tax credits are generated based on an amount of money invested. Others are generated based on an amount of production.

With federal tax subsidies so prevalent in today’s energy sector, understanding the details is critical.

In Part 1 of this series on the Section 45V clean hydrogen production tax credit (PTC), we reviewed the definition of “qualified clean hydrogen”. In Part 2, we introduced the concepts of lifecycle assessment and carbon intensity.

In Part 3, we reviewed the emissions associated with power production and their impact on tax credits. In Part 4 we turned our attention to natural gas.

Here, we consider how tax credits translate into actual economic value.

The Recap

The 2022 Inflation Reduction Act (IRA) created a new Section 45V PTC for clean hydrogen, with the credit amount ranging from $0.60 per kg to $3.00 per kg, depending on the carbon intensity of the hydrogen.

To determine the carbon intensity, the IRA requires a detailed assessment of lifecycle emissions, including feedstock supply, power supply, hydrogen production, and other aspects.

Tax Efficiency

Ultimately, the value of a tax credit is largely a question of timing. When will the credit be “monetized” – i.e., turned into actual cash proceeds or a reduction in cash going out the door?

Given the time value of money, tax credits that are monetized immediately are worth more. Tax credits that are monetized years in the future are worth less.

Until the passage of the IRA last August, most energy-related federal income tax credits were not “direct pay” – meaning the IRS would not send a refund check if the tax credit amount exceeded an entity’s tax liability. Most tax credits were also not “transferable”, meaning they could not be bought or sold.

Tax credits unable to be used in a given year would accumulate and “carry forward” for potential use in future years. The more years the credit has to be carried forward, the less valuable it is.

Projects or investors able to utilize tax credits as soon as they’re generated are said to be “tax efficient”. Those unable to take advantage of tax credits right away are said to be “tax inefficient”.

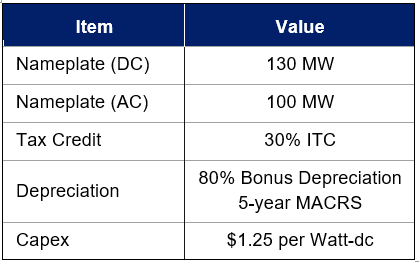

To illustrate the concept of tax efficiency, consider a hypothetical 100-megawatt (MW) solar project eligible for accelerated depreciation and a 30% investment tax credit (ITC) payable in Year 1 (see Table 1).

Table 1 – Example solar project

In a tax efficient scenario, the ITC and accelerated depreciation is worth approximately $70 million in present value. In an inefficient scenario, however, more than half of the tax benefits are lost (see Figure 1).

Figure 1 – Efficient vs. inefficient value of tax benefits

In the inefficient scenario, the ITC is carried forward and drawn down each year, resulting in no taxes owed but also no cash value. At the end of the allowable 22-year carryforward period, the remaining ITC balance expires.

Tax Equity

Traditionally, solar and wind projects have been developed by entities that don’t have significant tax liability to offset (called “tax capacity”) — often small teams of developers, not large corporations.

Seeking a solution, the renewable power industry embraced the concept of “tax equity”, which entails a developer partnering with a bank or other investor that can absorb the tax benefits.

In the US, partnerships are granted considerable leeway in how they allocate income and cash among the partners. Tax equity partnerships take advantage of this feature by allocating most of their income (i.e., the tax benefits) to the tax investor, while allocating most of the cash flow to the developer or “sponsor” (see Figure 2). The goal is to achieve as close to a fully tax efficient scenario as possible.

Figure 2 – Typical tax equity conceptual structure2

Figure 2 – Typical tax equity conceptual structure2

Tax equity structures have been critical to launching the US solar and wind industry, but they’re imperfect and notoriously complicated. Transaction costs can be high, and the sponsor cedes some value to the tax investor in exchange for its trouble. Even the most well-crafted tax equity structures result in some amount of lost value (called “leakage”).

Transferability

In addition to creating new tax credits, the IRA introduced a major change by allowing certain tax credits to be transferable and/or direct pay (see Table 21).

Table 2 – Energy-related tax credits in the IRA1

Table 2 – Energy-related tax credits in the IRA1

For transferable tax credits, purchasers will presumably demand a discount in exchange for their administrative requirements and any risk they’re assuming. The question, then, is what will this discount be?

We’ve seen some observers look to the transferable low-income housing tax credit (LIHTC) as a proxy. A relatively mature market exists for the LIHTC, and it has traded at around a 10% discount in recent years (see Figure 3). Others predict higher market discounts, particularly for projects requiring long development and construction durations.

Figure 3 – Historical pricing of LIHTC credits

Figure 3 – Historical pricing of LIHTC credits

One important point to remember is that the tax benefits of accelerated depreciation cannot be sold. So even with transferability, some amount of tax leakage will occur. For instance, the hypothetical solar project introduced earlier may still lose 20 percent or more of its tax benefits even if it sells the ITC (see Figure 4).

Figure 4 – Present value of example solar project tax benefits with transferability

Figure 4 – Present value of example solar project tax benefits with transferability

For this and other reasons, tax equity partnerships may still be the most economic option for many projects.

The IRA doesn’t appear to impose significant restrictions on who can purchase transferable tax credits, which introduces some intriguing possibilities. Will a clean hydrogen PTC mutual fund be an option someday for your 401k?

The IRS recently issued a Request for Comments3 on transferability, highlighting a number of key open questions. A few that we’re tracking include:

- In the case of partnerships, can the proceeds from the sale of tax credits be allocated however the partners choose?

- The IRA is clear that the proceeds from selling tax credits are not themselves subject to federal income tax, but will each state follow suit?

- Given they’ll be buying tax credits at a discount, will purchasers owe taxes on the associated gains they’ll be realizing?

Direct Pay

The renewable power industry has long sought direct pay as an alternative to tax equity. The IRA finally introduces it, but with significant caveats. For wind and solar projects, direct pay is limited to tax exempt entities and certain other specific groups such as the Tennessee Valley Authority (TVA).

For clean hydrogen (Section 45V), direct pay is available to all parties for the first five years of a project’s life. For the remaining five years of Section 45V’s applicability, the tax credits are transferable.

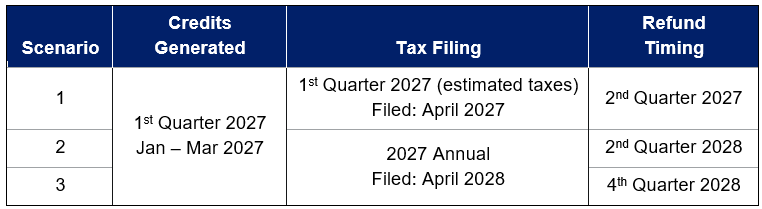

A key question for direct pay is: when will the proceeds (i.e., IRS refund checks) be available? Will the IRS generate direct pay refunds based on quarterly estimated tax filings, or will it require final annual filings? Once the IRS receives a tax filing, how long will it take to generate a refund? Will an audit be required first? Depending on the answers, the timing of actual IRS refund checks may be significantly staggered versus when the credits were generated (see Table 3).

Table 3 – Direct pay timing scenarios

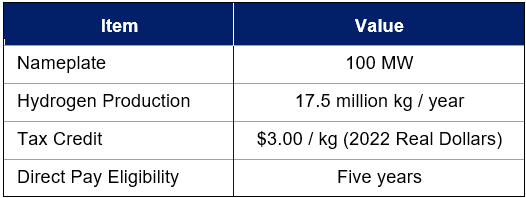

To illustrate the impact of direct pay timing, consider an example 100-MW project producing 17.5 million kilograms per year of green hydrogen (see Table 4). This project would be eligible for about $52 million per year of Section 45V tax credits (in 2022 real dollars).

Table 4 – Example green hydrogen project

The project’s $260 million of tax credits during the five-year direct pay period would have a present value of about $195 million. A quarterly direct pay scenario would be highly tax efficient, capturing more than 97 percent of the value. On the other hand, annual direct pay refunds the following December would be less than 90 percent tax efficient – a difference of $15 million in present value (see Figure 5).

Figure 5 – Present value of direct pay tax credits

Figure 5 – Present value of direct pay tax credits

Given the significant difference in value, it’s easy to see why many comment letters submitted to the IRS call for direct pay refunds based on quarterly estimated tax filings.

The Summary

Tax policy is an inherently complex subject, and tax credits are no different. With transferability and direct pay, the IRA introduces attractive new options for monetizing the clean energy subsidies. However, the actual economic value of these credits will depend on the detailed IRS regulations, which are due out by August. We’ll be following closely until then.

Contact us to discuss more.

Disclaimer:

The information in this blog has been provided by S&B for general information purposes. It does not constitute legal, accounting, tax or other professional advice or services and is presented without any representation or warranty as to the accuracy or completeness of the information. For advice relative to any of the categories stated, recipients should consult their own attorneys, accountants, or other professional advisors.

[1] Table 2 Source: 26 USC 6417 and 26 USC 6418

[2] Figure 2 Source: Novogradac LIHTC Equity Pricing Trends; https://www.novoco.com/resource-centers/affordable-housing-tax-credits/lihtc-equity-pricing-trends

[3] IRS Notice 2022-50; https://www.irs.gov/pub/irs-drop/n-22-50.pdf